How to Choose Between a Fixed & Variable Mortgage Rate

We've put together a framework to compare fixed and variable mortgage rates, including a calculator and a summary of what the experts are saying.

This year alone, 1.2 million Canadian households will be renewing their mortgage. That’s a lot of people staring at their screens, calculators in hand, asking: Should I go with a fixed or variable mortgage rate?

So, how do you make the right call? We’ve put together a framework to help, along with a calculator for those who want to get into the nitty-gritty. We end with a a look at what the experts are saying.

Fixed vs. Variable: What’s the Difference?

First, let’s define our terms:

Fixed Mortgage: A fixed mortgage rate remains constant for the entire term of the mortgage. Borrowers benefit from predictable payments, as their principal and interest portions do not fluctuate. This stability protects against interest rate increases but may result in higher initial rates compared to variable mortgages.

Variable Mortgage: A variable mortgage fluctuates based on changes in a benchmark rate, typically the lender’s prime rate, which follows the Bank of Canada’s policy interest rate. Variable rates tend to be lower initially but come with the risk of increasing costs if interest rates rise.

How do you decide?

The key factor is what happens to interest rates over the length of your mortgage. If rates fall and stay down, a variable mortgage is the way to go. If they rise, a fixed mortgage looks like a genius move in hindsight.

Of course, predicting interest rates three to five years out is a fool’s errand. Even the smartest economists in the country have difficulty predicting two years out.

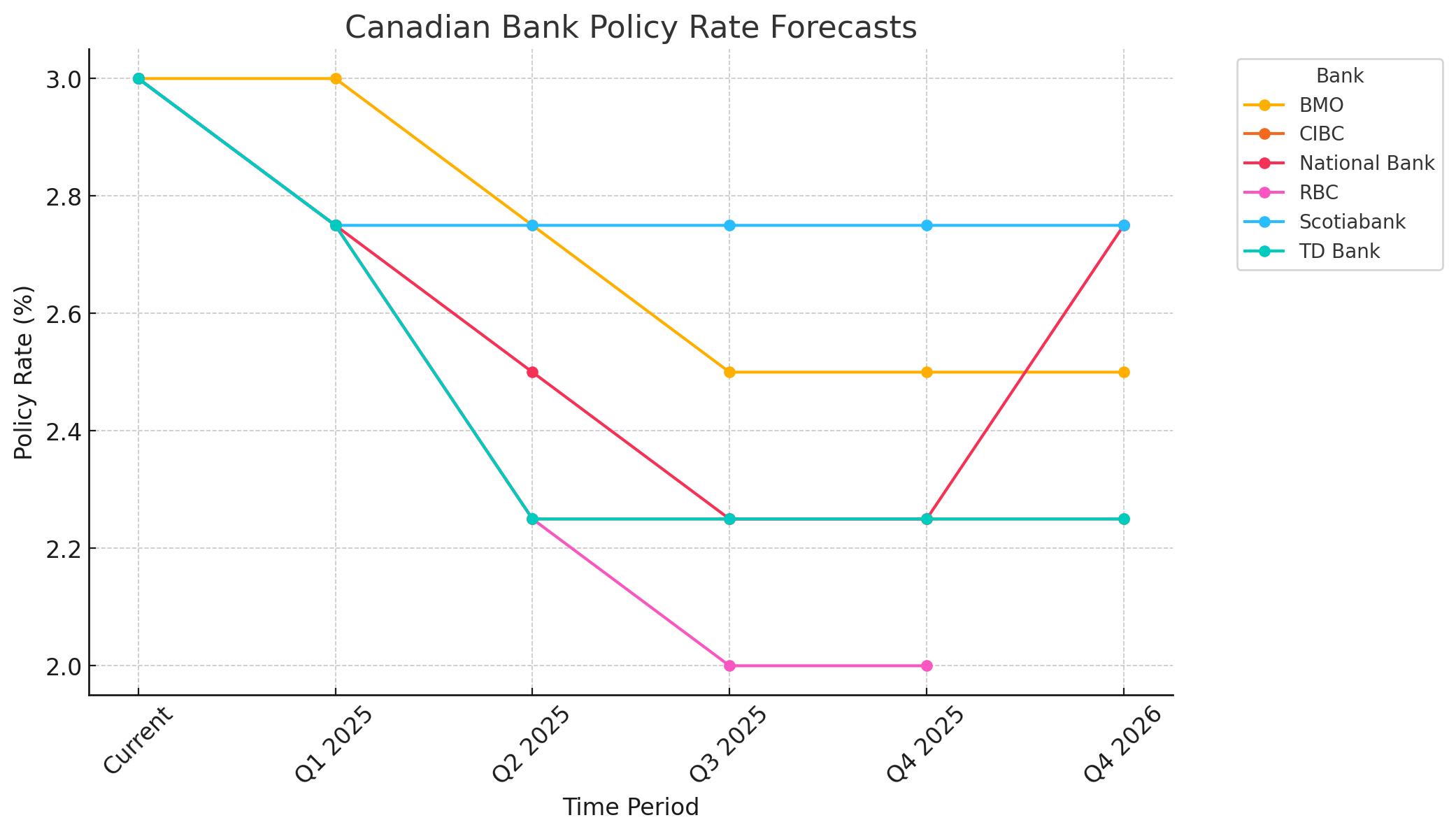

What we do have, however, is rate forecasts from Canada’s largest banks for the next two years. As you can see, most banks think rates will drop over the next couple of years.

A Calculator to Understand the Specifics

If you're looking to get more specific, this calculator from CMLS Financial is one of the best we've seen to compare fixed v. variable scenarios. Plug in your mortgage amount, amortization period, and rates to see how much you'd be paying under each scenario.

If we estimate a mortgage amount of $500,000, and compare:

- 5 year fixed rate of 4.04%

- 5 year variable rate of 4.15%, and

- assume BMO's policy rate forecast of a 0.25% cut in Q2 2025 and a further cut in Q3 2025 of 0.25%

The variable rate mortgage translates into a savings of $7,312 over the five year term. Remember, however, that this assumes the Bank of Canada rate won't increase in years 3-5 of the mortgage term.

So, What’s the Right Choice?

Sal Guatieri, BMO's a Senior Economist at BMO, similarly notes that if rates unfolds as expected, going with a variable rate mortgage would be worthwhile.

"We estimate a borrower putting 10% down on a half-million-dollar home financed over 25 years would save an average of [0.4%] per year compared with locking in for five years. That equates to just over $100 per month or more than $6000 in five years."

This is under the expectation that a trade war with the United States doesn't materialize. If a trade war does materialize, the Bank of Canada could reduce rates a further 1%-1.5%, leading to even more benefits for variable rate mortgage holders.

The good news is if you start with a variable mortgage and suddenly decide you'd rather not play the interest-rate guessing game anymore, you can switch to a fixed rate. The penalty for switching is typically 3 months of interest. The reverse, switching from fixed to variable, is typically much higher.

Ultimately, fixed mortgages give you certainty at a (typically) higher cost. Variable mortgages are cheaper upfront but come with risk. If you sleep better knowing your payments won’t change, go fixed. If you can tolerate some volatility and trust that rates will trend downward, go variable.